ASC 842 Lease Accounting: From Complexity to Clarity

Summary

×The implementation of ASC 842 has fundamentally transformed how organizations approach lease accounting. Gone are the days when operating leases could remain comfortably off balance sheet, hidden in the footnotes of financial statements. Today, nearly every lease must appear on the balance sheet as both a right of use asset and a lease liability. This change has sent finance teams scrambling to master present value calculations, classification criteria, and ongoing amortization schedules.

ASC 842 brings nearly all leases onto the balance sheet as ROU assets and liabilities

Yet beneath the surface complexity lies a systematic framework. ASC 842, while demanding, follows consistent mathematical principles that can be automated and streamlined. The challenge is not understanding the standard. It is managing the volume of calculations, tracking modifications across hundreds of leases, and ensuring every journal entry remains audit ready. This is where technology transforms compliance from a burden into a strategic advantage.

The Core Logic of Lease Measurement

The entire lease accounting process revolves around three critical phases: first determining the lease type, then calculating the initial value, and finally amortizing over the lease term. These three phases are interconnected and form the foundation of ASC 842 compliance.

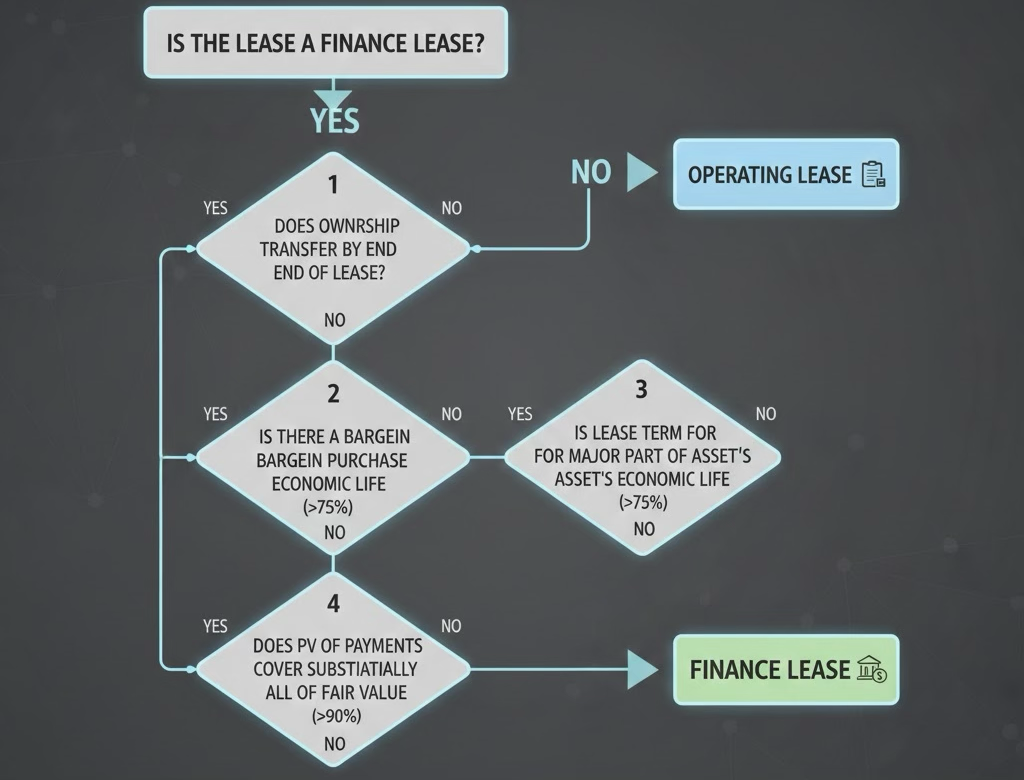

1. Understanding Lease Classification

Before any calculation begins, every lease must pass through the classification framework. ASC 842 maintains the distinction between finance leases and operating leases, and this determination drives everything that follows.

A lease is classified as a finance lease if it meets any one of five criteria: ownership transfers by lease end, a bargain purchase option exists, the lease term covers a major part of the asset's economic life, the present value of payments equals substantially all of the fair value, or the asset is highly specialized. If none apply, it's an operating lease.

The five classification criteria determine whether a lease is finance or operating

This classification decision is critical because it directly impacts the expense pattern on the income statement. Finance leases have higher expenses in early periods and lower expenses later, while operating lease expenses remain straight line constant.

2. Initial Measurement

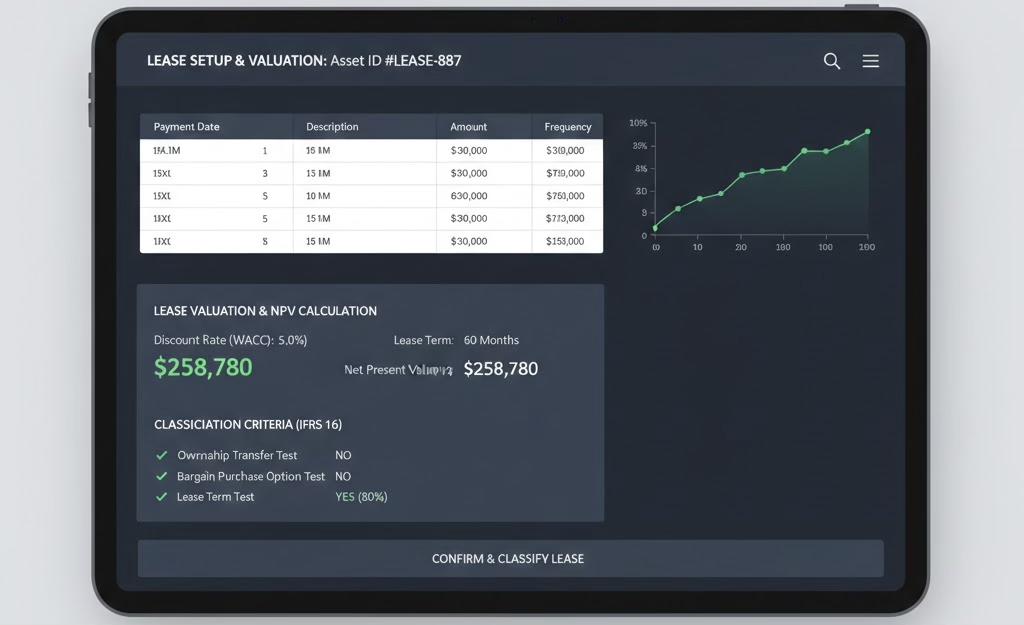

Once classified, the lease liability must be measured at the present value of future lease payments. This single number becomes the foundation for all subsequent accounting.

Let's look at a real example. Imagine you sign a 60 month equipment lease with monthly payments of $5,167, a 5.0% discount rate, and no initial direct costs or incentives. The net present value comes out to $258,780. That number becomes both your initial lease liability and the basis for your ROU asset.

The system automatically calculates NPV based on payment terms and discount rate

This calculation may seem straightforward, but when faced with irregular payment schedules, floating rates, residual value guarantees, or renewal options, the complexity and risk of error in manual calculations increase exponentially.

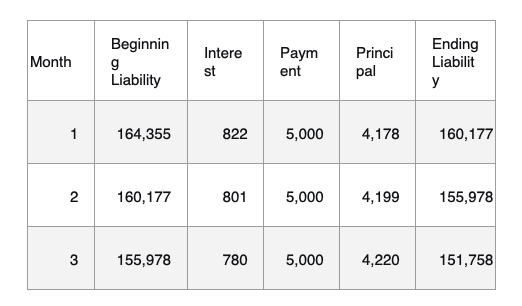

3. Subsequent Measurement

After initial recognition, the lease liability and ROU asset begin their respective amortization journeys, with the path depending on the lease classification.

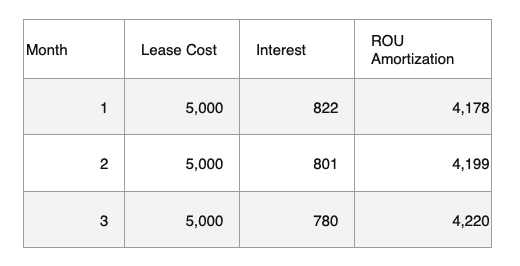

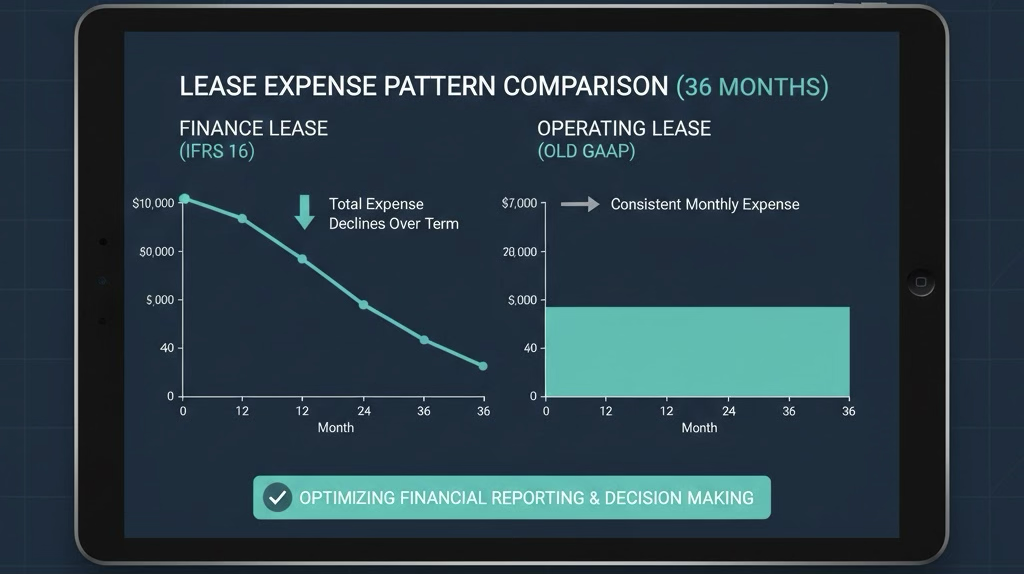

All lease liabilities are amortized using the effective interest method. Each month, interest accrues on the outstanding balance, and the payment reduces both interest and principal. Using a 36 month lease as an example:

The amortization path for the ROU asset varies by lease type. Under a finance lease, the ROU asset is amortized on a straight line basis, with total expense declining over time. Under an operating lease, the ROU asset is amortized as the difference between straight-line expense and interest, keeping total expense constant each period.

Finance leases show declining expense; operating leases show consistent expense

Handling Lease Modifications

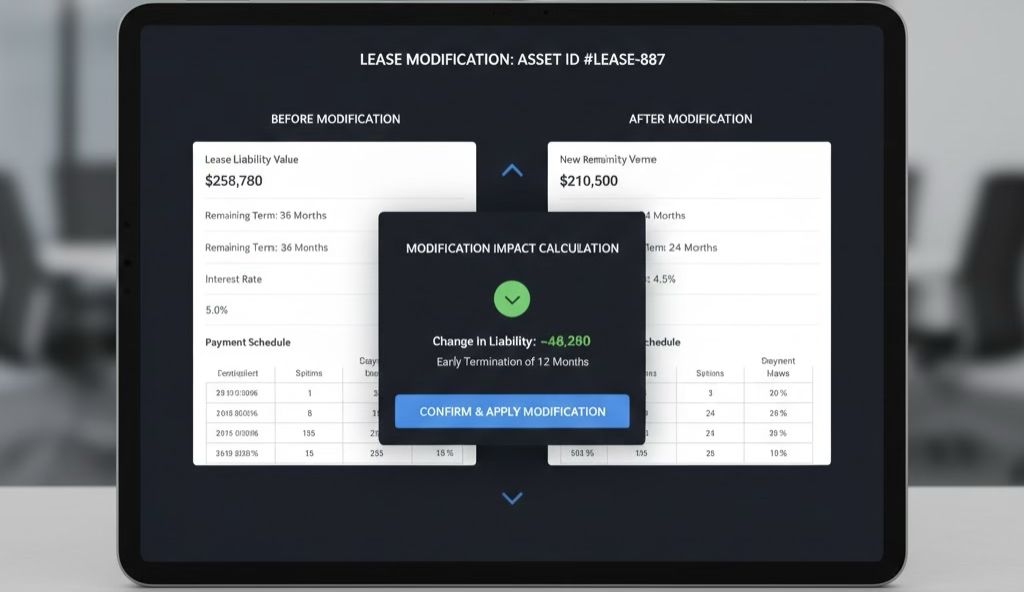

Real world leases rarely remain static. Options get exercised, terms get renegotiated, and spaces get vacated early, so each modification triggers remeasurement.

Common modification scenarios include renewal option exercise, early termination, and index based payment changes. For example, a lease with a $258,780 liability and 36 months remaining that terminates 12 months early would see its liability reduced by $48,280, with a corresponding reduction to the ROU asset.

Modifications trigger automatic remeasurement of liability and ROU asset

Handling these modifications manually is not only time consuming but also highly error prone; each remeasurement requires recalculating the amortization schedule and generating adjustment entries.

The Value of Automation Tools

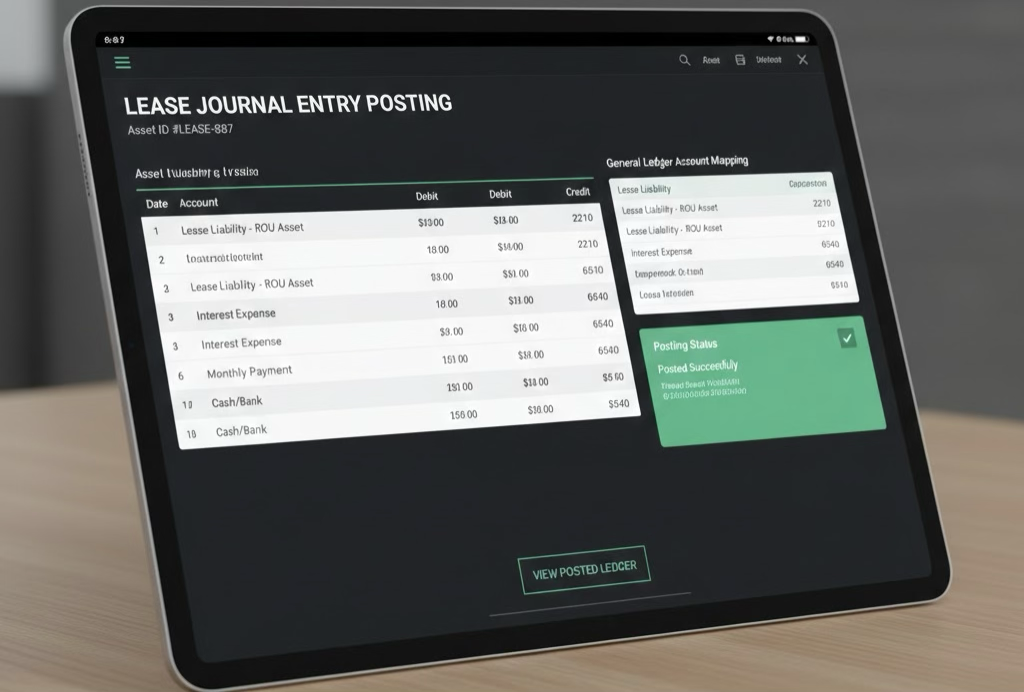

The ultimate output of all calculations is accurate, audit ready journal entries. At commencement, the ROU asset and lease liability are recorded. Each month, the system automatically generates entries for interest expense, principal reduction, and ROU amortization. These are all mapped to the correct general ledger accounts.

Automated entries ensure accuracy and auditability

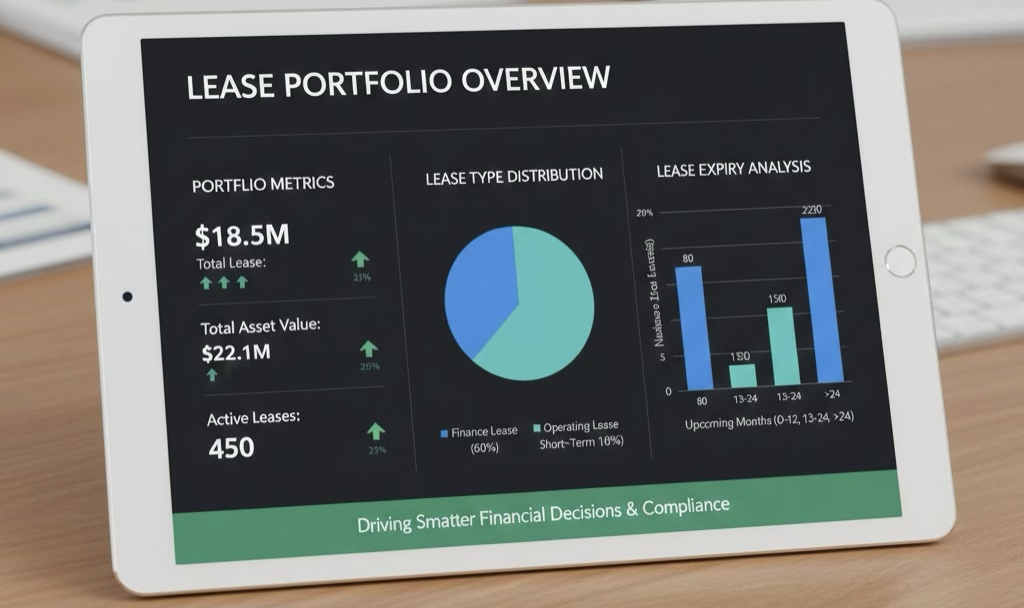

When the number of leases reaches hundreds, the portfolio view becomes as important as individual lease accuracy. Key metrics that managers need in real time include total lease liabilities, total ROU assets, active lease counts, distribution by type, and maturity analysis. All information required for ASC 842 disclosures can be generated instantly from the system.

Executive dashboard provides instant visibility into portfolio metrics

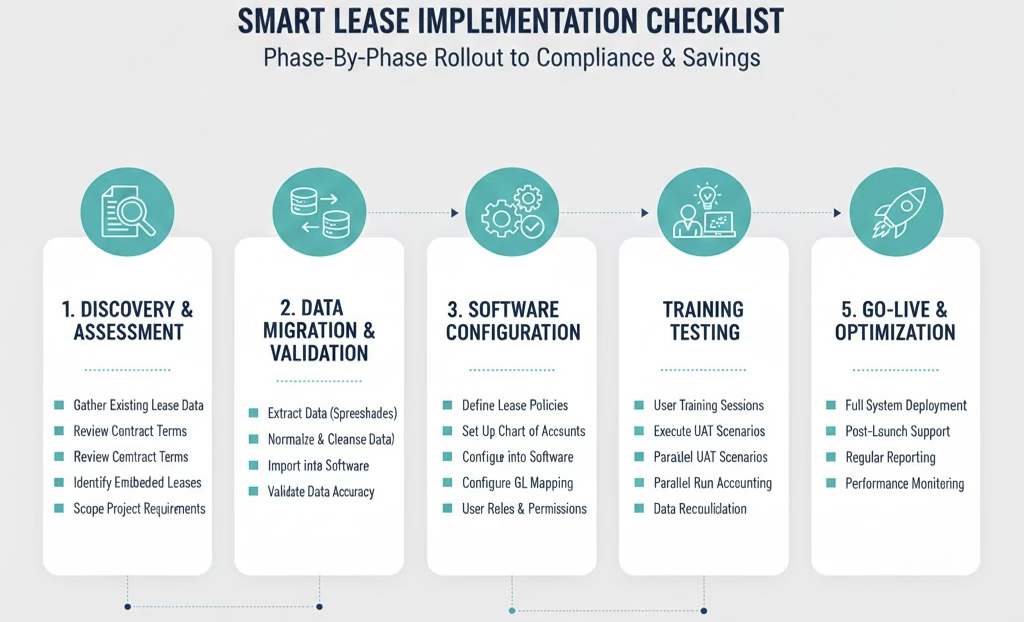

Implementation Roadmap

Successful ASC 842 compliance requires a structured approach. A complete implementation roadmap includes five phases: discovery and assessment, data migration and configuration, software training, go live and validation, and ongoing optimization. Each phase builds toward a fully compliant, efficiently managed lease portfolio.

A phased approach ensures smooth transition to ASC 842 compliance

Conclusion

ASC 842 need not be a source of anxiety for finance teams. While the standard introduces genuine complexity, these challenges are eminently solvable with the right approach.

Organizations that thrive under ASC 842 are those that recognize lease accounting as a systematic process rather than a periodic exercise. By automating calculations, standardizing modification workflows, and maintaining real time visibility into the lease portfolio, they transform compliance from a month end scramble into a continuous, reliable operation. For organizations managing significant lease portfolios, this is not just a matter of convenience; it is the defining factor between compliance risk and compliance confidence.

Ready to simplify your ASC 842 compliance? Contact our lease accounting specialists for a personalized demonstration.